BACKGROUND

THE PARTIES

On July 2nd, 2018, the Tax Court released its ruling in Roy E. Hahn, et al. v. Comm’r, TC Memo 2018-100. The case revolved around whether the taxpayers were entitled to deduct certain losses from a Custom Adjustable Rate Debt Structure (CARDS) transaction. The primary reason for this article is not to walk through the intricate details of an interesting and complex transaction, but instead to review the transaction in light of the economic substance doctrine and reflect upon current planning with such application of the doctrine in mind.

Petitioner, Roy E. Hahn, was a veteran tax professional with a background working with three predecessors of the big four accounting firms. Mr. Hahn had been in the tax world from 1974 to at least 2003 and was a CPA as well. Linda G. Montgomery had a similar background and had a CPA license and several years of experience working with a large tax firm. Hahn and Montgomery later formed Chenery Associates, Inc (“Chenery”) with each owning a 50% interest in Chenery.

Chenery, through much success, generated $4,346,254 in ordinary taxable income in the year 2000. Towards the end of the year, petitioners entered into a CARDS transaction in order to essentially eliminate this taxable income.

THE CARDS TRANSACTION

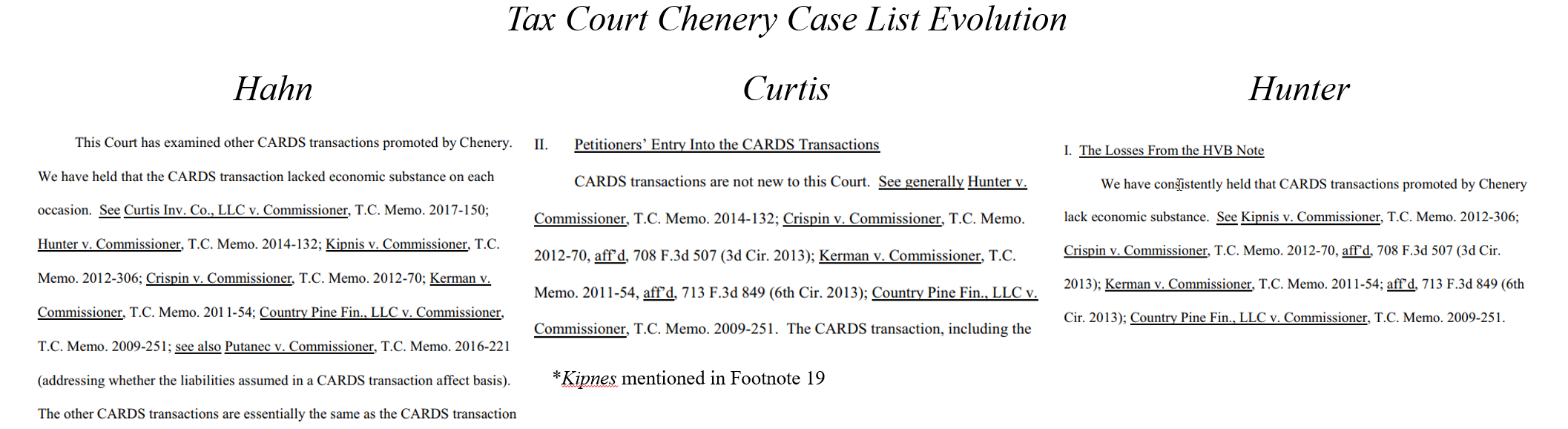

The CARDS transaction that is not new to the Tax Court, especially in relation to Chenery. In what one might call the Chenery cases, the Tax Court essentially made a list of the Chenery cases starting at the fifth case (Hunter) and adding to it in each subsequent opinion up to the Hahn (the seventh) case discussed here.1

The CARDS transaction generally has three stages:

- loan origination;

- loan assumption; and

- loan operation.

In November of 2000, Elizabeth Sylvester and Michael Sherry (UK Residents) formed Whitechapel Financial Trading, LLC (“Whitechapel”) in Delaware with nothing more than a few promissory notes. It was concluded that this formation was performed for the sole purpose of facilitating the CARDS transaction at issue. Shortly thereafter, the following steps were taken:

- Whitechapel applied for and received a loan from HVB Bank in Germany for € 5.8 Million;

- Whitechapel purchased a € 5.8 Million time deposit from HBV that accrued interest at .5% less than the loan;

- Chenery agreed to be jointly and severally liable on the HVB loan;

- Whitechapel distributed € 809,100 to Chenery;

- Chenery converted its distribution to USD at a 0.93 EUR/USD conversion rate;

- Chenery entered into a 1-year forward contract requiring Chenery to sell USD for EUR at 0.952 EUR/USD; and

- As the result of a claim of an inflated basis from the liability assumption, Chenery claimed a loss of $4,334,456 from the sale of the EUR Deposit (per Form 4797 on the Chenery 1120S).

![]()

Chenery treated the loss on the sale as ordinary under IRC § 988. The Tax Court disagreed stating that the transaction lacked economic substance.

ECONOMIC SUBSTANCE OF CARDS

To be respected, a transaction must have economic substance. The economic substance doctrine requires that a transaction have:

- Economic substance beyond just the creation of tax benefits (objective analysis); and

- A non-tax business purpose (subjective analysis).2 3

The economic substance doctrine was codified with Obamacare at IRC § 7701(o) in 2010 effective for transactions entered into after March 30, 2010.

In Hahn, the Court reviewed the transaction under the economic substance doctrine and found that under the objective test, the transaction lacked actual profit potential. The report referenced by the Court showed an actual projected net wealth reduction of $156,068 due to the fluctuations and contracts entered into. This was projected to be worse should the transaction extend beyond one year because the interest rates worked against the taxpayer coupled with the exchange rate fluctuations and cap on benefits due to the forward contracts. Considering the fees and financing costs, the IRS expert, Mr. Chodorow, concluded that the CARDS transaction offered no feasible possibility of a profit to the taxpayers. As such, the objective test was failed.

Under the subjective test, the petitioners argued that they intended to:

- profit from the EUR/USD conversion fluctuations;

- have access to loan proceeds in the future to invest in other investment opportunities; and

- invest in distressed assets with HVB.

The Court rejected this argument entirely. Particularly, the Court was offended by the fact that there was an argument to make a profit on the fluctuations when the taxpayers entered into contemporaneous forward contracts that would preclude pretty much any possibility to achieve a profit. The taxpayer essentially negated any chance to profit due to the forward contracts limiting any upswing in currency fluctuations that could have been favorable. Further, the Court was not persuaded about the credit facility usage and reminded the petitioners that they were aware that when they entered into the CARDS transaction, HVB did not have a hedge fund or any distressed assets available to invest in. The Court found there was no non-tax business purpose and determined the CARDS transaction lacked economic substance.4

ECONOMIC SUBSTANCE GENERALLY

When crafting a plan with tax aspects, it is increasingly important to remember that the transaction or plan must have substance beyond the tax benefits as well as non-tax business reasons. While each individual component of a transaction or plan may pass muster under the relevant sections of the law, the transaction as a whole must satisfy these requirements.

For transactions after March 30, 2010, the codified version of the economic substance doctrine requires:

- the transaction to change in a meaningful way (apart from income tax effects) the taxpayer’s economic position (Objective Test); and

- the taxpayer has a substantial purpose (apart from federal income tax effects) for entering into such transaction (Subjective Test).

CODIFICATION OF ECONOMIC SUBSTANCE

So, as seen above, the objective and subjective tests have been retained and codified in IRC § 7701(o). The law goes further to discuss profit potential. It is possible that a transaction may not be profitable during a snapshot of time in which a court may review it. The statute takes a net present value of benefits relative to present value expected tax benefits in determining profit potential.5 Also, financial accounting benefits are excluded from the analysis.6

WHY IS THIS IMPORTANT

When putting together a plan for a business that revolves around tax efficient structuring, it is important to note the business reasons for entering into the plan, the profit potential of the plan, and the motivation for entering into the plan. Doing so can help ensure the transaction, if reviewed, will be respected. Failure of the plan to be respected under these tests can result in an accuracy penalty of 40% of any of the resulting understatement of tax.7

CONCLUSION

While prudent planning is crucial in minimizing one’s tax liabilities, doing so just for the tax benefits can be problematic. As prudent planners, we like to work with clients to ensure that (1) transactions carry forward a valid profitable business purpose for our clients; and (2) the plan carries with it an efficient tax structure. Do not get lost in the tax minimization game so much that the reason for the underlying transaction is forgotten. Profit potential should independently support the transaction. In planning it must be remembered to not let the tax tail wag the dog. It can be easy at times for a plan to follow a tax designated track, but the underlying economics should be the primary factor for a taxpayer entering into any transaction, not just beneficial tax results.

Footnotes

- See Curtis Inv. Co., LLC. v. Comm’r, T.C. Memo. 2017-150, Hunter v. Comm’r, T.C. Memo 2014-132, Kipnis v. Comm’r, T.C.Memo. 2012-306, Crispin v. Comm’r, T.C. Memo. 2012-70, Kerman v. Comm’r, T.C. Memo. 2011-54, Country Pine Fin., LLC v. Commissioner, T.C. Memo 2009-251 (all involving Chenery and all holding CARDS lacked economic substance).

- Citing Reddam V. Comm’r, 755 F.3d 1051, 1059-1061 (9th Cir. 2014). This Case is applied in Hahn due to jurisdiction in the Ninth Circuit. It is applicable in the Tax Court in the case at hand under Golson.

- See also Klamath Strategic Inv. Fund. V. United States, 568 F.3d 537 (5th Cir. 2009) for pre-codification common law applicable to Fifth Circuit.

- The issue of the IRC § 6662(a) penalty (40% for non-economic substance transactions) was left for a future opinion to be issued by the Court. See Hahn v. Comm’r, TC Memo 2018-100 (Footnote 2).

- See IRC § 7701(o)(2)

- See IRC § 7701(o)(4)

- See IRC § 6662(i)